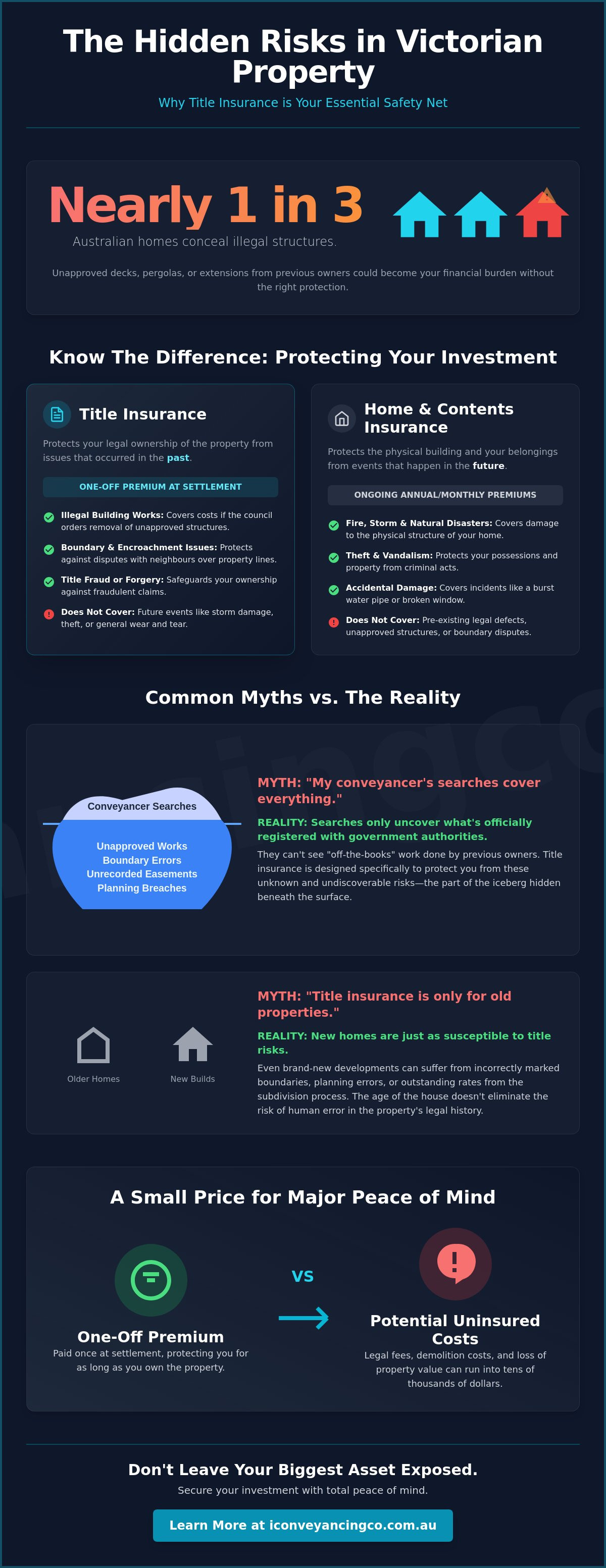

Did you know that nearly one in three Australian homes contain illegal structures like unapproved decks or pergolas? It's a staggering figure that highlights a hidden risk for anyone entering the Victorian property market in 2026. You might assume your legal checks cover everything, but the reality is that some issues stay hidden until long after you've moved in. This is where title insurance becomes an essential part of your purchase strategy.

Security. It's the foundation of a successful move. We understand the anxiety of potentially inheriting a previous owner's DIY mistakes or facing a sudden boundary dispute with a neighbour. While your conveyancer performs vital due diligence, title insurance acts as a vital safety net for risks that no search can uncover. This article debunks seven common myths to show you how a single, one-off premium protects your investment for as long as you own it. We'll clarify the confusion between home insurance and title protection to ensure you have total peace of mind throughout your property journey.

• Recognise how title insurance provides a permanent safety net for past property issues that standard home insurance policies won't cover.

• Identify the specific gaps in a Section 32 Statement and why vendor disclosures may not reveal the full history of illegal building works.

• Uncover the truth behind common myths, including why modern homes are just as susceptible to title risks as older Victorian properties.

• Learn how to safeguard your investment against costly boundary encroachments and council-ordered removals of unapproved structures.

• Gain clarity on how to weigh the cost of a single premium against the high-stakes financial impact of unknown legal defects.

Buying a home in Victoria involves a complex web of paperwork and legal checks. While your conveyancer works diligently to ensure the title is clear, some risks are simply invisible to the standard search process. Title insurance is a specialised policy designed to protect you from these hidden legal defects. It doesn't look at what might happen in the future, like a storm or a fire. Instead, it focuses on issues that already exist but haven't been discovered yet. This foundational article on What is Title Insurance? provides a neutral starting point for understanding how this protection functions globally.

In Victoria, our property market operates under the Torrens Title system. This system is generally robust, but it isn't infallible. Errors in the registry, fraud, or even mistakes made by previous owners can threaten your ownership. Title insurance steps in to provide a financial and legal shield for as long as you own the home. It's a unique form of indemnity because it can even extend to your heirs if they inherit the property from you. It ensures that the "legal right" to your land is as secure as the physical house itself.

Most insurance policies require monthly or annual payments to stay active. Title insurance is different. You pay a single premium at settlement, and that's it. There are no renewals and no ongoing administrative fees. This one-time investment covers you for the entire duration of your ownership. It's a permanent safety net. If a claim arises, most residential policies don't require an excess payment. This makes it a highly cost-effective way to manage risk. When you consider that legal battles over boundaries or illegal structures can cost tens of thousands of dollars, the modest upfront cost offers significant peace of mind. It removes the stress of future financial surprises related to your title.

It's common to confuse these two, but they serve very different purposes. Home and contents insurance protects the physical "bricks and mortar" from future accidents. If a pipe bursts or a tree falls on your roof, that's a future event covered by your standard policy. Title insurance covers your legal right to the land and the structures on it. It addresses "past" events. For example, if a previous owner built a garage over the boundary line ten years ago, home insurance won't help you when the neighbour demands its removal. Title insurance will. Think of home insurance as a shield against what might happen, while title insurance is a shield against what already happened but hasn't been found.

Misconceptions can be expensive in the Victorian property market. While most buyers focus on the physical condition of a house, legal risks often go unnoticed until it's too late. These myths create a false sense of security that can lead to significant financial loss. Understanding the reality of Is Title Insurance Worth It in Australia? helps you see past common industry jargon and protect your investment properly. Relying on outdated assumptions can leave you vulnerable to costs that no standard building inspection will catch.

Many buyers believe that because their conveyancer performs searches, title insurance is unnecessary. This is a misunderstanding of what a search actually does. Searches only reveal information that is officially registered with government authorities. They don't show work done "under the radar" by previous owners who skipped the permit process. Unknown unknowns, such as unrecorded easements or underground services not on the plan, are the primary reason for insurance. Even the most thorough professional cannot see through walls or verify the exact location of a boundary fence without a formal survey. Searches are about the record, but insurance is about the reality of the land.

There's a common belief that new homes in estates across Geelong or St Leonards are risk-free. This isn't true. Even in brand-new developments, errors occur. Developers might incorrectly peg boundaries, or there could be outstanding land tax and rates left over from the subdivision process. These issues don't disappear just because the house is fresh. This protection is equally valuable for vacant land purchases, where boundary disputes can stop a build before it even begins. Whether you're buying a period home or a modern townhouse, the legal risks remain consistent. Protection is about the title, not the age of the paint.

Some people assume they can simply sue the previous owner or the council if a problem arises. Litigation is slow, stressful, and incredibly expensive. You might spend years in court and tens of thousands in legal fees with no guarantee of success. In contrast, an insurance claim is designed to be a straightforward resolution. It provides a direct path to compensation or rectification without the need for a legal battle. If you're unsure about the specific risks of your next purchase, getting professional advice on buying properties conveyancing can help clarify your options before you sign the contract.

Understanding the specific protections of title insurance requires looking at the unique risks found in the Victorian property market. While the Section 32 Vendor Statement is designed to provide transparency, it often has gaps that only become apparent after the keys are handed over. This insurance is tailored to catch the risks that fall through these cracks, ensuring your investment remains secure against legal challenges. By adhering to Victorian property industry standards, buyers can better navigate these complexities with confidence and clarity.

The coverage is comprehensive and addresses several key areas that impact your financial security:

Protection against structures built without necessary permits from the local council.

Coverage for encroachments or incorrect fence placements that affect your land use.

Support when a property's current use violates local Geelong or Bellarine zoning regulations.

Security against inherited debts like land tax or council rates not settled by the vendor at the time of sale.

In regions like Geelong and the Bellarine, the "Geelong Pergola" scenario is a frequent issue. Imagine moving into your new home, only to receive a notice from the council stating your outdoor entertaining area was built without a permit by the previous owner. Under Victorian law, the current owner is often responsible for rectifying these issues. Local councils have the power to order the demolition of unapproved carports, decks, or pergolas. Title insurance typically covers the costs associated with these demolition or rectification orders. This protection often applies even if you suspected the structure might be unapproved at the time of purchase, providing a crucial financial buffer against council enforcement actions.

Older suburbs such as Geelong West or East Geelong frequently deal with "shifting fences." Over decades, fences are often replaced without a formal survey, leading to structures that slowly creep onto a neighbour's land or vice versa. These encroachments can lead to heated disputes and expensive legal battles when you try to sell or renovate. Your policy covers the legal costs of defending your right to the land or the physical cost of moving a fence to its correct position. For a deeper look at how these issues are identified during the settlement process, you can read our Conveyancer Geelong: Your 2026 Guide to Stress-Free Property Settlements. This ensures the physical boundaries of your property match the legal title you've paid for.

Inherited debts are another area where buyers feel the pinch. Occasionally, land tax adjustments or council rates are calculated incorrectly at settlement, or the vendor leaves behind a debt that the authorities then chase from the new owner. While your conveyancer does their best to clear these, errors in council records can happen. Title insurance provides a simple mechanism to clear these costs without you having to track down the previous owner. It maintains the financial predictability of your purchase, ensuring no hidden bills arrive in your letterbox months after moving in.

In Victoria, the Section 32 Statement is the cornerstone of property transparency. It's a legal requirement under the Sale of Land Act 1962, and recent changes under the Consumer Legislation Amendment Bill 2026 now require these statements to be available at least 14 days before an auction or sale. However, it's a mistake to view this document as a complete guarantee of a property's history. The statement is only as good as the information the vendor provides and the accuracy of the certificates attached to it. When these records fail, title insurance provides the necessary layer of protection that a standard legal review cannot offer.

A vendor is legally obligated to disclose what they know or ought to know about the property. This creates a significant grey area. If a previous owner performed illegal renovations decades ago, the current vendor might genuinely have no idea. They can't disclose what they don't know. Proving a vendor intentionally hid a defect after settlement is a difficult and costly legal exercise. You'd likely spend more on lawyers than the cost of the repair itself. Insurance bypasses this conflict. It offers a direct path to compensation without the need to prove fault or launch a lawsuit against the previous owner. It turns a potential legal battle into a straightforward claim process.

Administrative errors are more common than most buyers realise. Council databases aren't perfect. We've seen cases where a council certificate incorrectly states a property isn't in a flood zone or fails to list an outstanding building order. If you rely on that certificate and a problem surfaces later, the council's liability is often limited. Title insurance specifically covers losses that result from these administrative blunders. It ensures that an error by a government clerk doesn't become your financial burden.

Council records can be incomplete or contain errors that a standard conveyancing search won't flag. While you're checking for hidden issues, it's also wise to look at other potential costs. You can use our Land Tax Calculator Victoria: A 2026 Guide for Property Owners to ensure you're fully prepared for the financial side of ownership. This proactive approach helps you manage the "unknown unknowns" that can occur even with the best due diligence.

Relying solely on the Section 32 is a risk in a modern, fast-moving market. It's a vital tool, but it has boundaries. We help our clients navigate these gaps every day. If you want to ensure your purchase is fully protected before you commit, consider our expert pre-contract urgent Section 32's review service to identify risks early.

Deciding whether to invest in protection comes down to a simple risk-reward calculation. You are weighing a relatively small, one-off premium against the potential for a catastrophic financial loss. In the current 2026 market, the stakes are higher than ever for Victorian buyers. Local councils have significantly increased their use of drone surveillance and high-resolution aerial mapping to identify illegal building works. An unapproved pergola or deck that was hidden by a tall fence five years ago is now easily spotted by automated council audits. If a demolition order arrives, the cost of removal and the subsequent loss of property value can be devastating. Title insurance ensures that these modern enforcement methods don't result in an unexpected bill for thousands of dollars.

Every property has a different risk profile, but certain features should trigger a closer look at your insurance options. If you are nodding "yes" to any of the following, the argument for cover becomes much stronger:

Does the home have a deck, carport, shed, or swimming pool that might have been built without a permit?

Is the property over 10 years old, increasing the chance of multiple past owners making "under the radar" changes?

Do the fences look wonky, or do they seem to deviate from the straight lines of the street?

Is there evidence of recent work that may not have been fully signed off by a building inspector?

For most buyers, the "set and forget" nature of the policy makes it a logical choice. It's the only way to manage risks that are literally invisible during a standard settlement process.

We believe that property law shouldn't be stressful or confusing. Fiona Barber takes a calm and reliable approach to every settlement, ensuring that her clients in Geelong and the Bellarine Peninsula are fully protected from the start. We don't just process your paperwork; we act as your proactive partner in identifying potential title defects before they become your problem. We can arrange your policy as a seamless part of our buying properties conveyancing service, ensuring the premium is simply handled at settlement along with your other disbursements. This means you move into your new home with total confidence that your legal ownership is secure. Contact i.Conveyancing.Co today to ensure your Geelong property purchase is secured with expert advice and the right protection.

Your property journey should be defined by excitement, not anxiety over hidden legal defects. We've explored how title insurance serves as a permanent shield against the "unknown unknowns" that standard searches simply cannot find. From illegal structures to boundary encroachments, having a one-off policy ensures that your financial future remains protected for as long as you own your home. As Victorian councils embrace more advanced surveillance technology in 2026, this layer of security is no longer just an option; it's a strategic necessity for every savvy buyer.

Reliability. It's what we provide at i.Conveyancing.Co. Fiona Barber brings over 20 years of Victorian property experience to every settlement, offering personalised and transparent advice that lowers your stress levels. We specialise in Geelong and Bellarine Peninsula settlements, ensuring your transition into your new home is as smooth as possible. Don't leave your investment to chance when you can have a qualified expert on your side.

Secure your property investment with i.Conveyancing.Co’s expert support and move forward with total peace of mind. We're here to help you navigate the complexities of the market with clarity and ease. Your new beginning starts with the right protection.

No, title insurance is not a legal requirement for property buyers in Victoria. It is an optional but highly recommended layer of protection that works alongside your conveyancer's standard legal due diligence. While the law doesn't mandate it, many buyers choose it to manage the "unknown unknowns" that searches cannot uncover, providing a permanent safety net for a single one-off cost.

The cost is determined by your property's purchase price and is paid as a one-off premium at settlement. These premiums are tiered into specific brackets, such as homes valued under $500,000, between $500,001 and $750,000, and from $750,001 to $1 million. Higher tiers apply for properties up to $2 million and above. This single payment ensures your investment is protected for as long as you or your heirs own the property.

Yes, you can still obtain protection after you have moved in through an "existing owner" policy. While most buyers arrange their cover during the settlement process, you can apply for a policy at any time during your ownership. It's important to remember that the policy will not cover issues you were already aware of, so securing protection as early as possible is always the safest approach.

No, title insurance does not cover physical defects like termite damage, rising damp, or structural instability. These problems are the responsibility of building and pest inspections or your standard home and contents insurance. This specialised policy focuses exclusively on legal and ownership risks, such as zoning non-compliance, illegal building works, and boundary disputes that threaten your right to use the land.

As of June 2026, the two primary providers of this insurance in Victoria are First Title and Stewart Title Limited. Both companies offer comprehensive policies tailored for residential homes, strata units, and vacant land. Your conveyancer can help you understand the coverage options from these providers to ensure you choose a policy that matches your specific property type and risk profile.

If you discover an illegal pergola after moving in, your policy can cover the costs of demolition or rectification required by a council order. This includes the expense of physically removing the structure or the professional fees needed to seek retrospective approval from the authorities. This protection is a significant benefit for Geelong and Bellarine buyers, where unapproved outdoor structures are a frequent discovery after a sale.

Yes, the policy provides protection if a neighbour's structure or fence encroaches onto your land. If a dispute arises, the insurer can cover the legal costs of defending your title or the physical cost of moving the fence to its correct legal position. This is particularly useful in older suburbs where fences have often shifted over several decades without a formal survey to verify the boundaries.

No, a formal land survey is generally not required to obtain a residential policy. This is a major advantage for buyers, as professional surveys can be expensive and take weeks to complete. The insurance is designed to cover the risks that a survey would normally identify, such as incorrect boundary placements or encroachments, without requiring you to pay for an upfront inspection of the land's boundaries.